Hint: It Should Not

By Elham Saeidinezhad

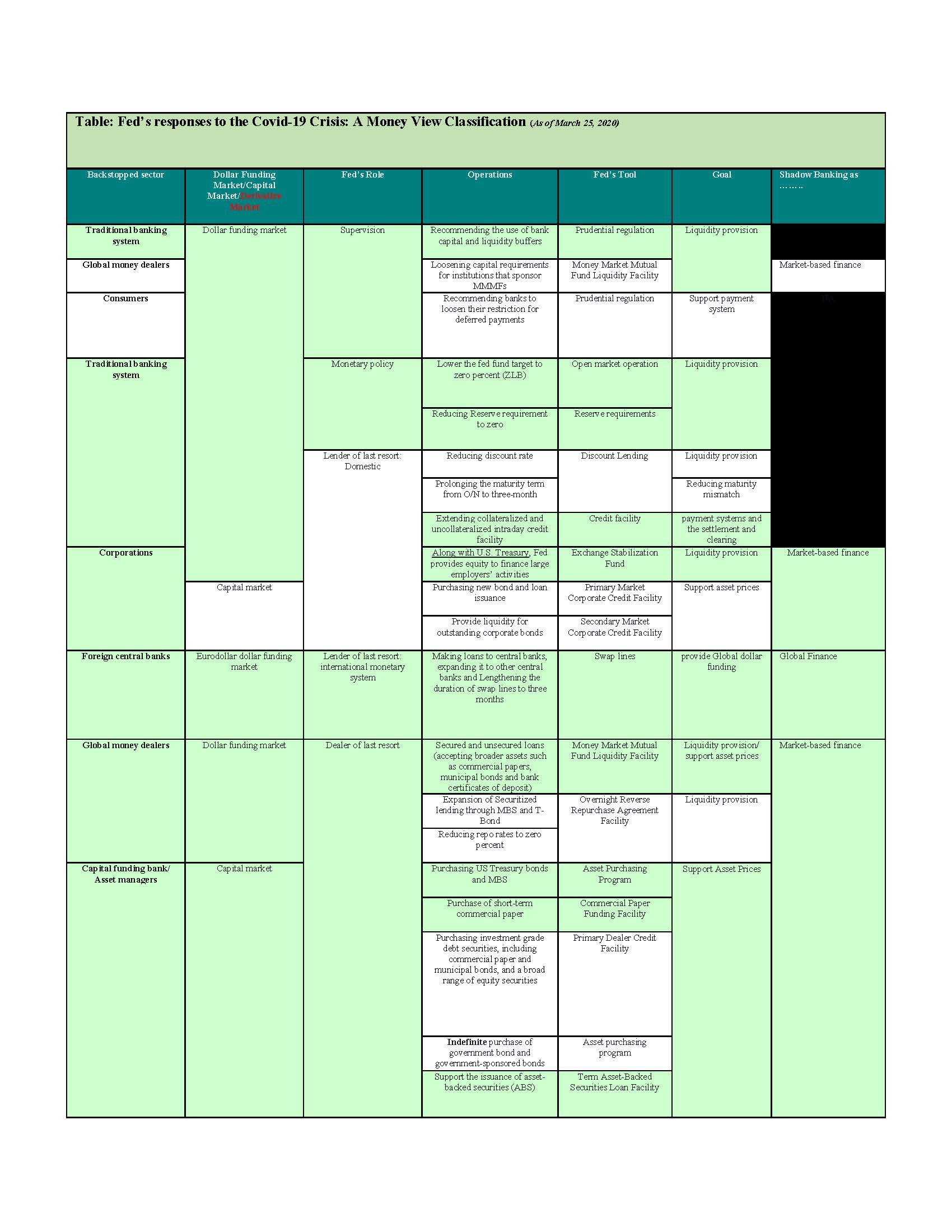

The unprecedented increase in the Fed’s involvement since the COVID-19 crisis has affected how financial markets function. The Fed has supported most corners of the financial market in an astonishingly short period. In the meantime, there have been growing anxieties that the Fed has not used its arsenals to help the derivatives market yet. To calm market sentiment, on March 27, 2020, regulatory agencies, led by the Fed, have taken steps to support market liquidity in the derivatives market by easing capital requirements for market makers- typically banks or investment banks. The agencies permit these firms to use a more indulgent methodology when measuring credit risk derivatives to account for the post-COVID-19 crisis credit loss. The goal is to encourage the provision of counterparty services to institutional hedgers while preventing dealers that are marginally solvent from becoming insolvent as a result of the increased counterparty credit exposure.

These are the facts, but how shall we understand them? These accommodative rulings reveal that from the Fed’s perspective, the primary function of derivatives contracts is a store of value. As stores of value, financial instruments are a form of long-term investment that is thought to be better than money. Over time, they generate increases in wealth that, on average, exceed those we can obtain from holding cash in most of its forms. If the value of these long-term assets falls, the primary threat to financial stability is an insolvency crisis. The insolvency crisis happens when the balance sheet is not symmetrical: the side that shows what the banks own, the Assets, is less valuable than Liabilities and Equity (i.e. banks’ capital). From the Fed’s point of view, this fearful asymmetry is the principal catastrophe that can happen due to current surge in the counterparty credit risk.

From the Money View perspective, what is most troubling about this entire debate, is the unrelenting emphasis on solvency, not liquidity, and the following implicit assumption of efficient markets. The underlying cause of this bias is dismissing the other two inherent functions of derivatives, which are means of payment and means of transferring risk. This is not an accident but rather a byproduct of dealer-free models that are based on the premises of the efficient market hypothesis. Standard asset pricing models consider derivative contracts as financial assets that in the future, can generate cash flows. Derivatives’ prices are equal to their “fundamental value,” which is the present value of these future cash flows. In this dealer-free world, the present is too short to have any time value and the current deviation of price from the fundamental value only indicates potential market dislocations. On the contrary, from a dealer-centric point of view, such as the Money View, daily price changes can be fatal as they may call into question how smoothly US dollar funding conditions are. In other words, short-term fluctuations in derivative prices are not merely temporary market dislocations. Rather, they show the state of dealers’ balance sheet capacities and their access to liquidity.

To keep us focused on liquidity, we start by Fischer Black and his revolutionary idea of finance and then turn to the Money View. From Fischer Black’s perspective, a financial asset, such as a long-term corporate bond, could be sold as at least three separate instruments. The asset itself can be used as collateral to provide the necessary funding liquidity. The other instrument is interest rate swaps (IRS) that would shift the interest rate risk. The third instrument is a credit default swap (CDS) that would transfer the risk of default from the issuer of the derivative to the derivative holder. Importantly, although most derivatives do not require any initial payment, investors must post margin daily to protect the counterparties from the price risk. For Fischer Black, the key to understanding a credit derivative is that it is the price of insurance on risky assets and is one of the determinants of the asset prices. Therefore, derivatives are instrumental to the success of the Fed’s interventions; to make the financial system work smoothly, there should be a robust mechanism for shifting both assets and the risks. By focusing on transferring risks and intra-day liquidity requirements, Fischer Black’s understanding of the derivatives market already echoes the premises of modern finance more than the Fed’s does.

The Money View starts where Fischer Black ended and extends his ideas to complete the big picture. Fischer Black considers derivatives chiefly as instruments for transferring risk. Money View, on the other hand, recognizes that there is hybridity between risk transfer and means of payment capacities of the derivatives. Further, the Money View uses analytical tools, such as balance sheet and Treynor Model, to shed new light on asset prices and derivatives. Using the Treynor Model to understand the economics of dealer’s function, this framework shows that asset prices are determined by the dealers’ inventory positions as well as their access to funding liquidity. Using balance sheets to translate derivatives, and their cash flow patterns, into parallel loans, the Money View demonstrates that the derivatives’ main role is cash flow management. In other words, derivatives’ primary function is to ensure that firms can continuously meet their survival constraint, both now and in the future.

The parallel loan construction treats derivatives, such as a CDS, as a swap of IOUs. The issuer of the derivatives makes periodic payments, as a kind of insurance premium, to the derivative dealers, who have long positions in those derivatives, whenever the debt issuer, makes periodic interest payment. The time pattern of the derivatives holders’ payments is the mirror image and the inverse of the debtors. This creates a counterparty risk for derivatives dealers. If the debtor defaults, the derivatives dealers face a loss as they must pay the liquidation value of the bond. Compared to the small periodic payments, the liquidation value is significant as it is equal to the face value. The recent announcements by the Fed and other regulatory agencies allow derivatives holders, especially banks and investment banks, to use a more relaxed approach when measuring counterparty credit risk. Put it differently, firms are allowed to keep less capital today to shield themselves against such losses in the future. Regulators’ primary concern is to uphold the value of banks’ assets to cement their solvent status.

Yet, from the point of view of the derivatives dealers who are sellers of these insurances, liquidity is the leading concern. It is possible to create portfolios of such swaps, which pool the idiosyncratic default risk so that the risk of the pool is less than the risk of each asset. This diversification reduces the counterparty “credit” risk even though it does not eliminate it. However, they are severely exposed to liquidity risk. These banks receive a stream of small payments but face the possibility of having to make a single large payment in the event of default. Liquidity risk is a dire threat during the COVID-19 crisis because of two intertwined forces. First, there is a heightened probability that we will see a cascade of defaults by the debtors aftermath of the crisis. These defaults imply that banks must be equipped to pay a considerable amount of money to the issuers of these derivatives. The second force that contributes to this liquidity risk is the possibility that the money market funding dries up, and the dealers cannot raise funding.

Derivatives have three functions. They act as stores of value, a means of payment, and a transfer of risk. Thus, they offer two of the three uses of money. Remember that money is a means of payment, a unit of account, and a store of value. But financial instruments have a third function that can make them very different from money: They allow for the transfer of risk. Regulators’ focus is mostly on one of these functions- store of value. The store of value implies that these financial instruments are reported as long-term assets on a company’s balance sheet and their main function is to transfer purchasing power into the future. When it comes to the derivatives market, regulators’ main concern is credit risks and the resulting long-term solvency problems. On the contrary, Money View uses the balance sheet approach to show the hybridity between means of payment and transferring risk functions of derivatives. This hybridity highlights that the firms use insurance instruments to shift the risk today and manage cash flow in the future. In this world, after a shock happens, it is access to liquidity, rather than the symmetry of the balance sheet, that keeps trading banks, and derivatives dealers, in business.

{kind=link}